Disruption Accelerated

KEY INSIGHTS

- The digitization of a wide range of industries and markets has accelerated during the coronavirus pandemic.

- Internet platforms perform better the more users they attract, resulting in powerful network effects and scale advantages.

- While we recognize the advantages of the largest firms, we take pains to research and meet with industry upstarts, which remain powerful sources of innovation and disruption.

The coronavirus pandemic has wreaked havoc across the global economy, and the technology sector has not been immune. Supply chains have come under pressure, and demand for many types of hardware and services has contracted as businesses postpone investment and consumers struggle. We have been meeting and collaborating—more recently, virtually—with the management teams of many of our holdings more than ever before as they seek to adjust to these unprecedented challenges.

But along with challenge has come opportunity—both for companies and investors. Many leading technology firms have continued to grow revenues and profits during the crisis, and some have even seen their stock prices reach new highs. As individuals around the globe work, shop, and consume entertainment at home, companies that provide the infrastructure for the online economy have seen demand for their services boom, allowing them to extend their dominance.

While some of the shift online is likely to reverse as shopping malls, offices, and movie theaters reopen, we suspect that many of the changes we have seen in recent months will remain permanent. Working from home full time will likely become more common, for example, especially now that 300 million people have experienced videoconferencing through Zoom. And many millions more have had their first experiences shopping for groceries online and seem likely to value the convenience even after health concerns have abated. In our view, the current crisis—like many before it—has only accelerated changes that were already underway.1

All Businesses Must Digitize

Especially with many people unable or reluctant to leave home, companies of all sizes and across nearly every industry are realizing the importance of having a digital relationship with their customers. Whether they are retail shoppers or business partners, customers want the ability to search for products and track purchases online. For their part, companies find that interacting online with customers brings powerful efficiencies and cost savings while allowing them to gather valuable data about evolving consumer demands and preferences.

"Firms that achieve the necessary scale can then learn faster, gather more data, and further improve their products..."

But merely collecting data and maintaining an online presence is not enough. Companies must be able to organize massive data sets before they can extract useful insights while guaranteeing that their websites and customer service processes always function flawlessly. Firms must also secure and protect strategic data, which is one reason cybersecurity is the fastest‑growing category of information technology (IT) spending. The challenge is to focus on companies making the investments that will drive real returns.

The Platform Companies Have Extended Their Dominance

In this new digitized world, scale is crucial. Companies with the most capital to deploy can invest in the latest technology, which in turn attracts more customers. Firms that achieve the necessary scale can then learn faster, gather more data, and further improve their products—helping attract additional customers, boosting returns, and allowing for further investment. The positive feedback continues, resulting in enormous growth for some companies while disrupting markets.

The tech giants that have best embodied this phenomenon are the world’s leading platform companies—a list that typically includes Facebook, Alphabet (Google), Apple, and Amazon.com in the U.S. and Alibaba and Tencent in China. These companies have pioneered a new business model not only by using the internet to sell their products and services, but also by operating digital communities that connect buyers with sellers as well as content creators with an audience. These platforms have offered more value as they have attracted more users—a classic example of what are termed “network effects.” Few seeking to track down an old friend would turn anywhere but to Facebook, for example, while most looking for an obscure kitchen gadget would first turn to Amazon.

The Platform Model Is Spreading

Online computing resources offered by Amazon Web Services, Microsoft’s Azure, and others have fostered the development of the cloud‑based software industry. Software‑as‑a‑service (SaaS) providers operate on a subscription basis and allow customers to adjust their software spending up or down to match the evolving needs of their business. Freed from the need to pay for complex software packages they may never use—as well as the servers and support staff needed to run and service them—companies can invest instead in a more productive capacity. It is no wonder that the largest and most successful SaaS companies have very high customer retention rates.

One trend we have noted in recent Silicon Valley visits is that some of the dominant SaaS firms are pursuing the platform model. A primary example is ServiceNow, a leading provider of software aimed at helping companies automate workflows and manage their IT infrastructure. The company’s new Now Platform enables customers to build their own workflow applications using simple “drag‑and‑drop” tools, dispensing with the need for complex coding. The Now Platform’s flexibility and ease of use has the potential to extend the customer base beyond the IT department.

Leading Semiconductor Firms Benefit From Improving Industry Structure

The leading players in the semiconductor industry have also grown more dominant over the past decade. In part, this reflects the impact of the 2008 global financial crisis, which sparked a dramatic rationalization in capacity and resulted in an entirely restructured industry. In the memory market, we have seen the number of major global players dwindle to three or four in the DRAM and NAND markets, respectively. The consolidation has given the remaining players more leverage in dealing with customers and the potential for better margins in a tamed supply cycle. Growing demand from the hyperscale data centers that serve the cloud should provide a powerful tailwind for these well‑positioned firms.

Tremendous consolidation has also occurred in the market for analog semiconductors, even as demand for these chips that convert light, temperature, and other physical signals into digital ones appears poised to accelerate. Driving the growth is the proliferation of the internet of things, which is seeing chips built into a range of smart devices. The auto industry is an especially voracious consumer of analog chips, and its appetite is only likely to grow as more electric and autonomous vehicles take to the road. Broader end markets for semiconductor firms help diversify revenues, potentially leading to more durable growth and returns.

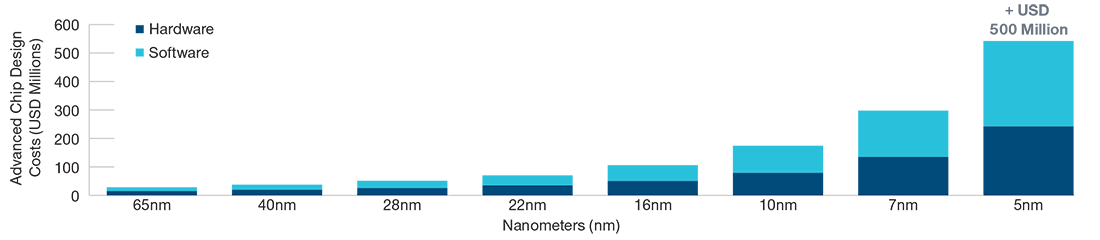

CAPITAL INTENSITY HAS BEEN GROWING IN SEMICONDUCTOR INDUSTRY

(Fig. 1) The cost of designing chips has increased rapidly as laws of physics are tested.

As of July 2018.

Source: Synopsys—IBS July 2018 report.

Leading‑edge chips are manufactured using progressively smaller manufacturing processes, represented in nanometers (nm).

Power semiconductors, which regulate the flow of electricity in a device, are also proliferating throughout the digitized economy. Germany’s Infineon Technologies is the world’s largest producer of these chips, which are heavily used in industrial power control systems and are increasingly important in the automotive industry. It is the second‑largest supplier of chips to automakers.

The Challenges of Leading‑Edge Chip Design

Growing demand for leading‑edge chips to power compute‑intensive workflows and the rising costs associated with producing these advanced semiconductors give an important potential advantage to a select set of leading firms—a group of “linchpin” companies, as we describe them. Capital intensity in the industry is increasing as firms invest heavily in new production techniques and equipment, allowing for the extension of “Moore’s law”—the 50‑year pattern of regularly doubling the number of transistors that can fit on a chip.

We believe one example of such a firm is Synopsys, a leader in electronic design automation software that engineers rely on to understand how the billions of components on a chip will work together. As the laws of physics become more challenging in fabricating advanced chips, we believe cutting‑edge equipment and software technologies will be indispensable. Together, the improved industry structure, the spread of chips into ever more devices, and the new challenges in manufacturing have created a sector with the potential for higher returns.

"...the improved industry structure, the spread of chips into ever more devices, and the new challenges in manufacturing have created a sector with the potential for higher returns."

Media and the New “Network” Effects

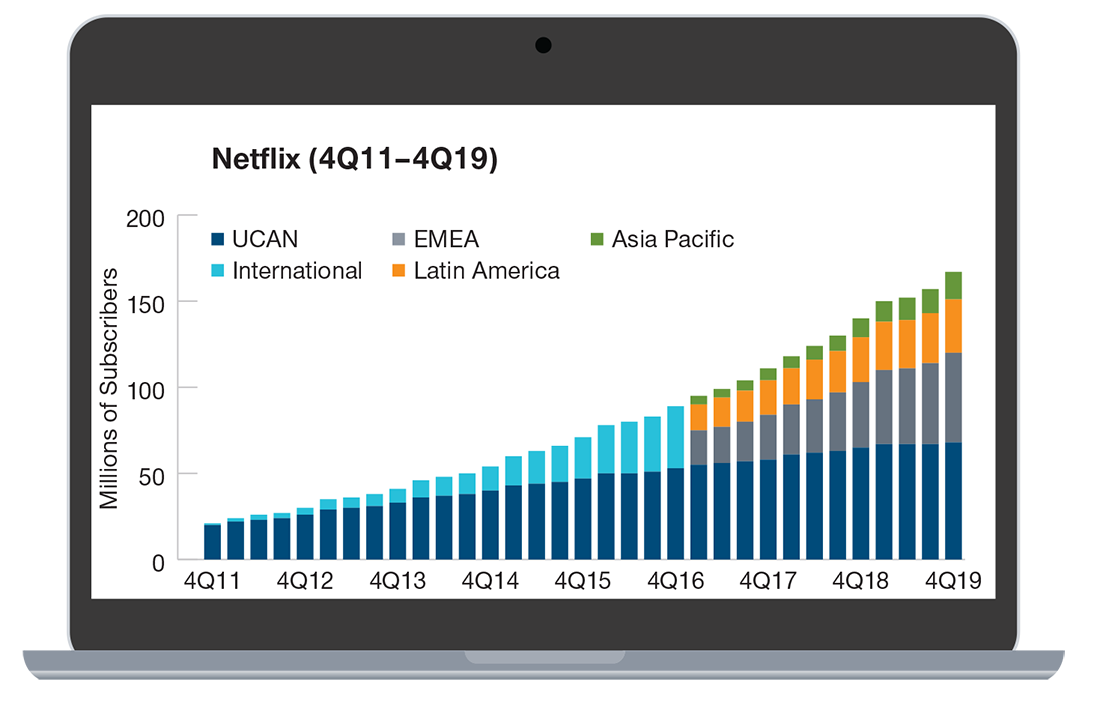

Along with advertisers and retailers, the media industry has been upended by online platforms that offer an improved customer experience. The primary disruptor has been Netflix, which counted 167 million subscribers at the end of 2019. Unlike traditional broadcasters, Netflix is not constrained by borders, and the company has been seeing its fastest growth in international markets. The company’s massive subscriber base and robust data capabilities allowed Netflix to be the first to perceive new viewership trends and create content that targets them—as shown by the company’s success in developing highly relevant original movies and television shows.

The streaming market has been flooded with other competitors over the past few years, but we believe that only the largest players are likely to survive. Walt Disney is late to the game but has the resources to operate on a multinational scale—and may seek to leverage its intellectual property online even more now that its theme parks are shut down. Apple and Amazon’s Prime service may also prove to be durable competitors, but we believe that most subscribers may treat these as add‑ons to their core Netflix account. Interestingly, the coronavirus pandemic has strengthened Netflix’s hand against its rivals. With production sets shut down, Netflix has been able to draw on its huge, multinational library of previously filmed content.

NETFLIX’S “NETWORK” EFFECTS

(Fig. 2) A global footprint gives it a lead on the competition.

As of December 31, 2019.

Sources: Company filings. Netflix international subscribers breakout data only available beginning 1Q17.

AI May Also Favor the Largest Internet Companies

The companies that seem likely to dominate artificial intelligence (AI) will, in our view, have three attributes: the best computing power, the largest data sets, and the best data scientists—all characteristics of today’s leading platform companies, which are already making important strides in the field. Google was a pioneer in AI, and the company is now developing tensor processing units, a new type of chip designed for neural networks, computing systems designed to mimic brain functions. Netflix and other consumer‑oriented platforms are deploying AI and machine learning in developing better content, along with more precise recommendations for users and better ad targeting.

"...the interesting question for investors may not be how the big internet companies compete in AI, but how AI spreads to other industries."

Indeed, we expect that the internet giants might eventually provide AI as a sort of on‑demand infrastructure. A company might send an unstructured data set to Google or Amazon, for example, which would then deploy one of its algorithms to clean up the data and help guide customers to make better decisions. Here, too, the interesting question for investors may not be how the big internet companies compete in AI, but how AI spreads to other industries. We are keeping an especially close eye on how AI will change the financial services industry, and T. Rowe Price is investing in and harvesting its potential.

With the Tech Giants Likely Only to Get Bigger, Is Regulation a Threat?

Amazon.com, Facebook, Google, and other dominant platform companies have drawn scrutiny for their size and the breadth of the markets they are targeting. The impact of the coronavirus pandemic is further proof of this trend, which we expect to continue. However, we believe it is far from clear that, unlike Ma Bell and other dominant firms in history, today’s platforms are stifling innovation and harming the consumer. Indeed, the opposite may be true: The “Amazon effect” has brought down retail prices, and popular services such as Google Maps or Instagram are free. Appreciation for the services provided by the platform companies during the pandemic has also changed the tone of the conversation, at least temporarily.

But is the concentration of so much market power still a threat? Regulators, politicians, and judges may come to different conclusions, and investors will have to pay attention as the debate continues. We are also mindful that any new regulatory frameworks could end up benefiting the largest companies, as smaller companies can’t typically bear new compliance burdens.

We Don’t Ignore the Upstarts

Despite the advantages of some of the largest firms, investors may find some of the best investment opportunities in younger and smaller companies. In part, this is because the war chests of the industry’s giants have grown so dramatically that they can afford to snatch up promising upstarts at healthy premiums.

Takeover potential is one reason we conduct extensive research into the swelling private market for technology companies. But exploring opportunities in private companies also improves our understanding of competitive dynamics and helps provide us the earliest possible awareness of changes in the ecosystem. In many cases, we are able to position ourselves as partners with these companies and get to know them in advance of going public. When a company completes its initial public offering, our familiarity with its strengths and opportunity can help us act quickly, potentially resulting in a better outcome for our clients.

Even as the world struggles with the pandemic, the rapid pace of innovation continues, and the powerful secular growth trends that we expect to create value in the technology sector remain intact. It appears that we are still relatively early in a golden age for technology innovation, as the extraordinary power of the internet has enabled unprecedented value creation for both companies and investors.

WHAT WE’RE WATCHING NEXT

While tech giants are playing a prominent role in the digitization of the economy, smaller companies are exploiting emerging areas where online services are making communicating and transacting easier. Twilio is a leader in cloud‑based tools that enable enterprises to embed voice, video, and chat communications into their applications. For its part, Shopify is a cloud‑based software company that provides an online commerce platform for small to midsize businesses. Meanwhile, Zendesk has emerged as a leading provider of cloud‑based customer service and engagement platforms for rapidly growing business‑to‑consumer operations. Being on the right side of change means identifying and investing tactically in companies that make it easier for businesses of all sizes and across the economy to expand their online presence, improve productivity, and engage customers across multiple channels.

1 The specific examples mentioned throughout were chosen to illustrate our thinking about industry and corporate trends.

The companies mentioned above represented the following allocations in the Global Technology Fund as of March 31, 2020: Alibaba Group Holding: 8.6%; Amazon.com: 6.5%; Netflix: 5.5%; Facebook, 4.4%; ServiceNow: 3.2%; Alphabet: 2.7%; Tencent Holdings: 1.9%; Zendesk: 1.4%; Synopsys: 1.3%; Microsoft: 1.1%; Shopify: 1.0%; Zoom Video Communications: 0.8%; Infineon Technologies: 0.7%; Twilio: 0.6%.

Important Information

Call 1-800-225-5132 to request a prospectus or summary prospectus; each includes investment objectives, risks, fees, expenses, and other information you should read and consider carefully before investing.

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

The views contained herein are those of the authors as of May 2020 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

Investing in technology stocks entails specific risks, including the potential for wide variations in performance and usually wide price swings, up and down. Technology companies can be affected by, among other things, intense competition, government regulation, earnings disappointments, dependency on patent protection and rapid obsolescence of products and services due to technological innovations or changing consumer preferences. Investing in private companies involves greater risk than investing in stocks of established publicly traded companies. These risks may include less available information, illiquidity and difficulty in valuating private companies.

This information is not intended to reflect a current or past recommendation, investment advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Investors will need to consider their own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Investment Services, Inc.

© 2020 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

Drew Propson: Head of Technology and Innovation in Financial Services at the World Economic Forum

In this episode, Drew provides her global perspective on how technology is shaping the future of wealth management, which tech driven solutions have been overhyped, and which are underrated!

Accelerating the WealthTech Transformation

An Envestnet report illuminating opportunities ahead. 5 key themes for 2021 and beyond.

Joel Bruckenstein and Bob Veres: From WealthTech’s effect on Advice to Survival of the “Most Authentic”

In this episode, The industry legends share top insights and learnings from their recently released Technology Survey and how they impact industry trends overall, provide guidance to advisors of all sizes and more.