How to Enhance Performance and Income in Bond Strategies

While the recent rise in interest rates has provided near-term relief, historically low interest rates continue to stifle bond income and investors are seeking other ways to generate return and outperform. But they struggle with limited options — bets related to either credit quality or duration. This, in turn, limits potential for outperformance. However, the options are expanding. Our research shows that a technique to drive outperformance in equity strategies also shows promise for bond strategies.

The Limited Bond Investing Toolbox

We’ve found that investors’ overweights or underweights to duration and corporate credit versus a market benchmark drive upwards of 70%* of the variation in bond manager excess returns**. Duration is how much a bond price moves when interest rates move. The price of a higher duration bond, which usually has a longer term maturity, rises and contributes more to returns when interest rates decline. Credit is associated with a company’s financial performance. A company’s bond price will rise if it performs better financially than most investors expect. In essence, driving outperformance in the bond world largely comes down to pulling just these two levers.

These limitations exacerbate the already low income investors receive from bonds, depressing total return, because of persistently low interest rates. Yield across bond classes — including high yield, U.S. and European government, investment grade, and emerging market bonds — are near multi-decade lows. Understandably, investors are seeking alternative ways to generate return and outperform with their bond investments.

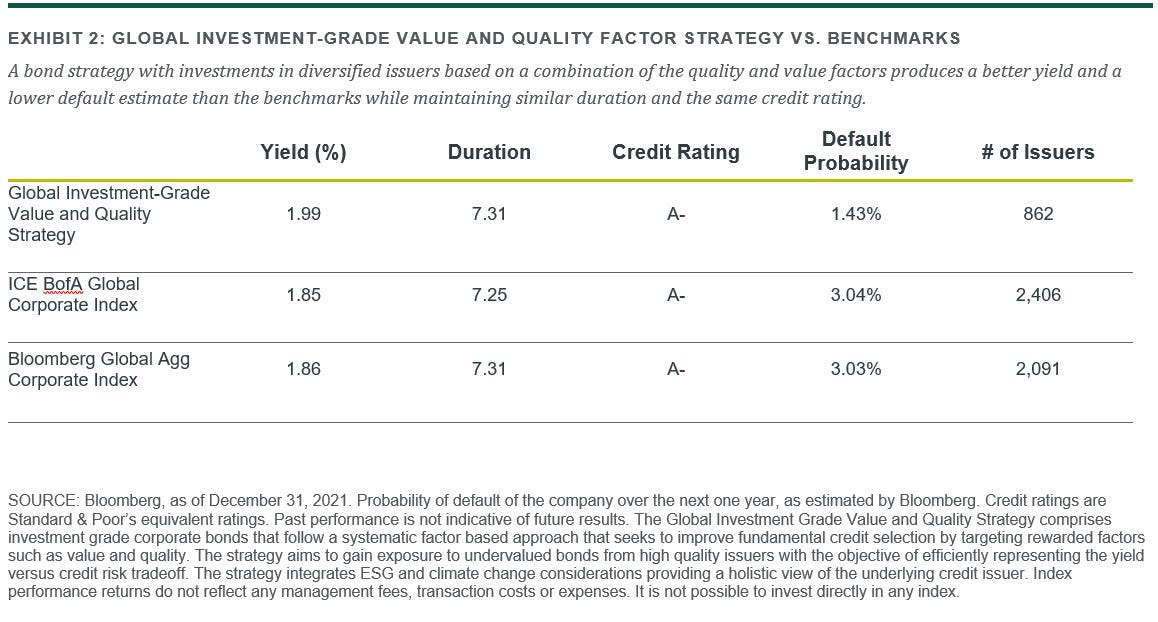

Applying a Proven Path to Historical Outperformance

Investors will discover such an alternative across the proverbial financial- markets pond in the stock market. Academic studies and our research show that, over the long-term, some types of stock with certain characteristics called factors^ consistently outperformed the stock market on a risk adjusted basis. Factor-based investing is a form of systematic investing that involves selecting securities based on characteristics that are associated with higher expectations of excess returns. These factors can be broadly categorized as low volatility, high quality, high dividend, value, small caps and momentum. Recent academic studies have found that bonds with most factors also have outperformed.^^

By selecting bonds based on these factors, we believe investors can construct strategies that generate competitive income without taking more risk. Exhibit 2 shows an investment grade strategy invested in bonds with strong quality and value characteristics. The strategy provides a higher yield with a lower default estimate than benchmarks with similar average durations and credit ratings. In other words, the strategy boosts income and lowers risk through factor investing while remaining neutral in other areas. This positioning forms the hallmark of any factor-based strategy. Investors focus on taking risk-efficient bets that pay (factors) while otherwise intentionally positioning their strategies close to the benchmark with sector weightings, credit rating, duration and other areas.

Factor Performance for High Yield Bonds

The effectiveness of factor-based investing extends into other bond sectors. Exhibit 3 shows that some factors have historically outperformed in particular in the high yield bond market. Investors can use strategies of a single factor or multiple factors to achieve targeted outcomes. Importantly, they should consider liquidity with factors such as momentum, in which high turnover can trigger trading costs that eat into returns.

A Larger Bond Investing Toolbox

Factors, standing on the shoulders of decades of empirical research, expand bond investors’ options to enhance performance with consistent risk-adjusted returns. In an environment where every basis point of return matters and opportunities to generate income are challenging, we believe investors should consider applying factor-based investing strategies to their fixed income portfolios.

Explore factor-based investing at Northern Trust Asset Management.

See our latest insights and research.

*Mehta, Azeredo, Good Luck or Skill: Can fixed income managers time market environments? (2021), Mladina, Peter, Bond-Market Risk Factors and Manager Performance (September 2019). Khan, Ronald, and Lemmon, Michael. “Smart Beta: The Owner’s Manuel.” The Journal of Portfolio Management(Winter 2015).

**Excess returns above the one-month Treasury bill rate

^Mehra, Rajnish; Edward C. Prescott (1985). “The Equity Premium: A Puzzle”. Journal of Monetary Economics 15 (2): 145–161. Carhart, M. M. (1997). “On Persistence in Mutual Fund Performance”. The Journal of Finance 52: 57–82. Goyal, A. and Sunil Wahal (2008). “The Selection and Termination of Investment Management Firms by Plan Sponsors”. Journal of Finance 63: 1805–1847.

^^Mehta, Hunstad(2017), Looking Beyond Term and Credit: Factors that drive performance of European Corporate Bonds. Israel, R., Palhares, D., and Richardson, S. (2016), Common Factors in Corporate Bond and Bond Fund Returns, Bektic, D. & Neugebauer, U. & Wegener, M. & Wenzler, J.-S., 2017. “Common Equity Factors in Corporate Bond Markets,” Publications of Darmstadt Technical University, Institute for Business Studies (BWL)

IMPORTANT INFORMATION. For Asia-Pacific markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. Northern Trust and its affiliates may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Opinions and forecasts discussed are those of the author, do not necessarily reflect the views of Northern Trust and are subject to change without notice.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. Information is subject to change based on market or other conditions.

Forward-looking statements and assumptions are Northern Trust’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Past performance is no guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by Northern Trust. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For additional information on fees, please refer to Part 2a of the Form ADV or consult a Northern Trust representative.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Belvedere Advisors LLC and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A.

P-031522–2072413–031523

Weekly Investment Commentary: Munis offer yield relief from inflation’s heat

U.S. yields began the year at their highest starting level since 2011, and they have since risen further across the Treasury and municipal curves.

Global Weekly Commentary: Higher bar for U.S. earnings to deliver

We saw 2024 as a year of two stories. First, cooling inflation and solid corporate earnings would support upbeat risk appetite.

Global Markets Weekly Update: April 19, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.