Selectivity Drives Success in Health Care Sector

Key Insights

- Regulatory worries weighed on the health care sector early in 2019, but the most innovative companies continue to thrive.

- Drug development is accelerating thanks to genomics and other breakthroughs, and we are seeking to identify potential winners among small and mid‑size companies.

- We are overweight in the small life sciences tool segment, which historically has tended to outperform late in the market cycle.

After outperforming the broader market in 2018, health care shares struggled for much of the first half of 2019 due to concerns over a possible U.S. “Medicare for all” system and drug price regulation. Breaking down the sector into its component parts reveals a different story, however. Shares in many of the most innovative companies have performed well in recent months. Moreover, we believe companies producing leading‑edge therapeutics and medical devices offer some of the market’s most attractive growth areas for investors with a multiyear horizon.

Our Focus on Innovation

In the Health Sciences Fund, we look for companies that discover and develop medicines and therapeutic devices that we believe address patients’ unmet needs and can improve their lives. On the services side, we are interested in providers that can offer better access to health care or lower health care costs. While we are sensitive to valuations, we look for companies with sustainable growth rates. Accordingly, many of our holdings—especially those working on promising new medicines—are likely to be regarded as growth stocks. These innovative companies can be found across all subsectors of the health care sector, allowing us to maintain a well‑diversified portfolio.

We also prefer smaller companies, particularly within the therapeutics space, as they tend to benefit more from successful product launches than larger, mature companies. While this approach can increase volatility at the individual stock level due to the binary nature of clinical drug trials, we seek to manage this risk by limiting position sizes. As potential therapies successfully clear clinical hurdles, we may increase our positions as the risks decline.

We believe our large staff of analysts with extensive medical and scientific backgrounds—I personally can draw on my former experience as a physician—gives us an edge in conducting careful fundamental research on firms of all sizes. Company visits, industry conferences, and other research potentially enable us to develop insights into growth drivers that other investors might miss. Our research relies on much more than just our ability to read to a financial statement or go over a balance sheet.

"The good news for health care investors is that drug innovation appears to be accelerating…"

Genomics Is Driving a New Wave of Drug Development

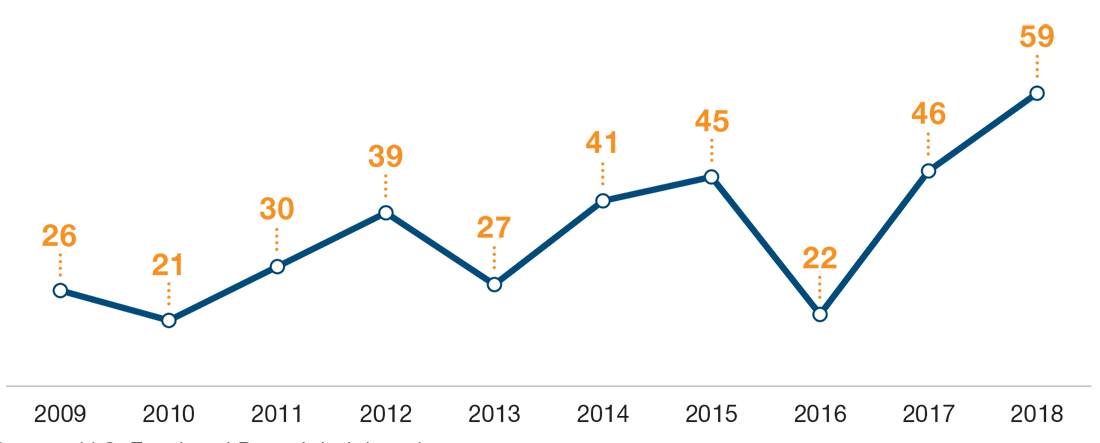

The good news for health care investors is that drug innovation appears to be accelerating, as evidenced by 59 new drug approvals by the U.S. Food and Drug Administration’s Center for Drug Evaluation and Research (CDER) last year. Progress in gene therapy is an important driver of new drug development. The cost of sequencing an individual’s genome has declined to roughly USD 100, compared with over USD 1 million a little over a decade ago. Companies are taking information gleaned from genomics to develop targeted therapies that can attack cancer cells or pathogens such as viruses while leaving healthy cells untouched. Genomics also helps companies better understand how an individual will respond to a particular drug.

Sage Therapeutics is developing treatments for central nervous system diseases. As of this writing, it is preparing to launch the first‑ever drug for postpartum depression, which afflicts about 10% of all new mothers. The drug involves a new mechanism that can resolve symptoms rapidly—within a day—and provide lasting relief to patients. It could end up treating a variety of forms of depression and even insomnia—potentially multibillion‑dollar markets. With a market capitalization of almost USD 9 billion, Sage is a mid‑cap company. However, we bought it when it was a small‑cap stock.

The falling costs of gene research allow smaller and newer companies to make important advances. We recently sold our position in Spark Therapeutics, which was acquired by Roche Holding in an all‑cash transaction for over USD 4 billion. Founded in 2013, Spark offers a platform for Roche to develop a range of new therapies for genetic conditions such as hemophilia and retinal disease.

With the advent of electronic medical records and the use of powerful software and computing engines to process “big data,” drug companies can also conduct population studies much more quickly and cheaply. Based on the genome sequencing of a single family with very high cholesterol, for example, Amgen and Regeneron Pharmaceuticals have developed powerful new cholesterol‑regulating drugs.

(FIG. 1) NEW DRUG APPROVALS ARE ACCELERATING

Annual Novel Drug Approvals by the CDER, 2009 Through 2018

Source: U.S. Food and Drug Administration.

T. ROWE PRICE BEYOND THE NUMBERS

Private Company Investing

An extension of our investment process

Our deep and experienced health care team allows us to invest in areas where there isn’t a lot of coverage by Wall Street analysts. In some cases, this may include investing in private companies. We view private investing as simply an extension of our investment process. In our view, we have the resources to evaluate early‑stage pipeline companies and analyze them from a researcher’s perspective to understand what their potential success rate might be in the future and determine whether we believe they can transition into durable‑growth companies and generate attractive overall returns.

While private investments represent a small percentage of the Health Sciences Fund portfolio, they potentially provide us with valuable industry insights and innovation trends that we believe advantage all our investment efforts.

New Devices and Analytical Tools Offer Opportunities

Innovation is also accelerating in the medical devices industry. One standout firm is Intuitive Surgical, maker of the da Vinci surgical system, a minimally invasive surgical robot operated by a doctor sitting nearby. Intuitive’s robots are rapidly being adopted in surgical centers around the world, and we’re excited about the company’s new product line. Robotic surgery is also poised to get a boost from the arrival of lightning‑fast 5G wireless networks, which promises to make operations conducted remotely safer and more common.

The life science tools industry is the smallest sector in both our fund and our benchmark (the Lipper Health/Biotechnology Funds Index), but it is one in which we are overweight and where we see good potential. This diverse subsector includes companies that make analytical tools and other equipment, along with a range of clinical and research services. Illumina is the dominant provider of next‑generation DNA sequencing technologies, which we believe is the best long‑term growth driver in the industry. We also like the subsector because it tends to perform well late in the market cycle. Illumina, Danaher, Thermo Fisher Scientific, and other market‑leading companies generate ample cash, which they can use to buy back stock or make acquisitions.

"While a transition to a single‑payer health care system would indeed upend the health insurance industry, such a change is likely to take years, if it happens at all."

Service Providers Struggle Under Regulatory Worries, but Opportunities Remain

We have benefited lately from being underweight in the health care services segment, which has come under a cloud of regulatory uncertainty following calls from Bernie Sanders and other presidential candidates for a single‑payer health care system. While a transition to a single‑payer system would indeed upend the health insurance industry, such a change is likely to take years, if it happens at all. The fundamental earnings backdrop for these companies also remains robust. Nevertheless, we expect services stocks may struggle until the results of the Democratic primaries become clear.

Meanwhile, there seems to be broader momentum for increased government support for managed care, and we’re invested in companies—such as Humana, Anthem, and UnitedHealth Group—that offer Medicare Advantage programs. The U.S. likely will need these private companies to manage health care services and costs, whatever share of the cost the government pays. Health care services stocks have recently traded at a roughly 20% discount to the overall market, creating selective opportunities for those of us with the patience to wait for the regulatory turbulence to subside.

20%: Health care services stocks’ recent discount to the overall market

While the health care sector faces heightened political risk as the 2020 election cycle approaches, our longer‑term view on the sector remains positive because of tailwinds related to aging populations, clinical needs, and accelerating innovation. However, we believe investors need to be selective and focus on identifying companies developing innovative, game‑changing therapies and those offering cost‑effective, quality health care services that can create value over the long term.

What We Are Watching Next

In our view, the medical technology industry is benefiting from a number of tailwinds, including favorable demographics, an accommodative regulatory environment, and continued innovation driving new product cycles. Exact Sciences provides an accurate and easy‑to‑use, noninvasive screening test for colorectal cancer and precancerous lesions. We believe the company is in the early stages of adoption for its cancer screenings, providing a long runway for growth as the firm makes progress in penetrating its approximately USD 5 billion addressable market.

The fund’s top 10 holdings as of June 30, 2019 were as follows: UnitedHealth Group, 5.8%; Intuitive Surgical, 4.7%; Becton, Dickinson & Company, 4.7%; Vertex Pharmaceuticals, 3.7%; Thermo Fisher Scientific, 3.6%; Stryker, 2.9%; Pfizer, 2.9%; SAGE Therapeutics, 2.6%; Anthem, 2.5%; Danaher, 2.2%. Among other holdings listed above, Roche Holding represented 1.3%; Amgen, 1.2%; Regeneron Pharmaceuticals, 1.2%; Illumina, 0.7%; Humana, 1.1%; and Exact Sciences, 0.8%. Spark Therapeutics was not held in the portfolio.

Important Information

Call 1-800-225-5132 to request a prospectus or summary prospectus; each includes investment objectives, risks, fees, expenses, and other information you should read and consider carefully before investing.

The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for the portfolio, and no assumptions should be made that the securities identified and discussed were or will be profitable.

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

The views contained herein are those of the authors as of July 2019 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

The fund is subject to market risk, as well as risks associated with unfavorable currency exchange rates and political economic uncertainty abroad.

This information is not intended to reflect a current or past recommendation, investment advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Investors will need to consider their own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. Due to the fund’s concentration in health sciences companies, its share price will be more volatile than that of more diversified funds. Further, these firms are often dependent on government funding and regulation and are vulnerable to product liability lawsuits and competition from low-cost generic products. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Investment Services, Inc.

© 2019 T. Rowe Price. All rights reserved. T. Rowe Price, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

Peeling back the onion: A concentric approach to investment decision making

Portfolio Managers Greg Wilensky and Jeremiah Buckley offer a framework for interpreting economic news for investment decision making.

What is ESG and why do we care?

Michelle Dunstan, Janus Henderson’s Chief Responsibility Officer, explores ESG considerations and highlights how ESG integration helps Janus Henderson deliver on client goals and aspirations.

Hiding in plain sight: The investment case for healthcare

Though healthcare may have flown under the market’s radar this year, the sector’s attractive valuations and new growth opportunities are not to be overlooked, say Portfolio Managers Andy Acker and Dan Lyons.