report by BlackRock

Student of the Market: October 2023

As the 2020 election season heats up and President Trump’s odds of winning continue to run cold, we believe it is important to understand the investment implications of a potential change in government versus the status quo. We have outlined the policy implications of the three most likely election outcomes: a Democratic sweep, a Biden presidency with a Republican Senate and a Trump presidency with a Republican Senate. This analysis assumes that Democrats hold the House, which we believe is highly likely.

After a lengthy vetting process, Democratic presidential candidate Joe Biden selected Senator Kamala Harris as his running mate for the 2020 presidential election. Though many names were floated in the past month, Harris has long been considered a favorite for the VP pick. Harris, a 2020 candidate for president herself, fits the bill as an experienced politician with liberal credentials and a knack for fundraising. In the past Biden spoke about the need to pick a VP who could lead the country if needed, and her experience in California state government and the U.S. Senate, as well as her national profile, make her a natural choice.

For many, economics is viewed only through the lens of numbers. But what can economics teach us about planning and making life decisions?

Russ Roberts joins the podcast to discuss the intersection of economics and life. From embracing uncertainty to evaluating financial tradeoffs, Russ will help broaden your perspective and apply economic principles to your clients’ daily lives.

In our view, the markets feel much healthier at the end of April than a month ago, but underappreciated in the improved sentiment is not only the scale of March policy action, but its continuation into April. Actions announced in April would ordinarily have remained in headlines and discussion for weeks, but the nearly half trillion dollar U.S. fiscal stimulus package has been treated almost as a footnote to its much larger cousin in March. Similarly, Fed and other central banks not only continued to implement the massive programs initiated last month, but significantly expanded on them.

As the first country to tackle COVID-19, China has institutional investors globally wondering about the local situation – and what it means for their portfolios. June Lui, Portfolio Manager, BMO LGM Investments, gives an on-the-ground assessment of China’s economic backdrop and the impact on stocks.

This is a hard commentary to write. The situation is obviously very grave but also extremely fluid and no one has any special or privileged insight as to when a degree of normality may return. All pandemics end but it would be foolish on our part to suggest that it will be over within a few months. What is clear is that the world is tumbling into a serious global recession with significant unemployment. When both supply and demand collapse the end result is obvious and unavoidable. Governments and central banks have thrown several kitchen sinks at the crisis but with a world in lock-down it does little to lift economic activity. Expenses go up but incomes go down.

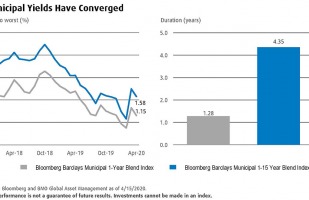

Over the past several weeks, yields between short- and intermediate-term Municipal Bonds have converged. This may be an opportunity for investors to significantly reduce interest rate risk while sacrificing minimal income since shorter-term bonds typically have less sensitivity to rates.

2020 began largely as we expected from an economic perspective, but as the first quarter ended it was difficult even to remember what “normal” economic times looked like, that is, before COVID-19 mushroomed and became a global health crisis.

Before the situation deteriorated in late February, many economists expected the economic effects of the virus to be primarily felt in the first and second quarters with a “v-shaped” recovery to follow. Now many expect a “u-shaped” recovery occurring perhaps by year-end. Economic indicators can lag the headlines, but U.S. unemployment had already begun to spike as the first quarter ended with more to come, likely climbing to double digits as large segments of the economy remain shut down in an effort to contain the virus. We have seen second-quarter annualized GDP estimates ranging from -5% to -30%, but the unprecedented combination of a pandemic and the modern global economy makes this very difficult to call. The numbers will be painful, regardless of the precise magnitude. In terms of the human cost, the pain is already acute.

Credit markets have seen extreme repricing over the past month as a result of the market stress caused by coronavirus and its impact to the economy. The period through March 26 saw some of the most aggressive corporate spread widening in history, with the worst days experiencing almost twice as much widening as any day in 2008. Global investment grade corporate credit spreads reached 340 basis points after having started the year at 102, and we saw global high yield spreads widen past 1,000 basis points as an index, which is generally the level considered the threshold for individual bonds to be considered part of distressed indices.

As the global spread of COVID-19 continues, the United States’ timeline to practice social distancing has now been extended through the end of April. The crisis continues to evolve, leading to questions of how long the social distance measures will remain, how severe will the infection rate get, and when will peak cases be reached. Gauging the length of these measures is crucial to anticipate the economic impacts to U.S. businesses and consumers.

Initiatives such as Veganuary and meat-free Mondays are a sign of how patterns of food consumption are changing. People are increasingly aware that their eating habits can come with dramatic environmental and social costs. As investors, we are particularly interested in how companies are managing ESG risks in both their operations and supply chains, as well as whether they are seeking opportunities in high-growth areas such as vegan protein.

What caused the extreme municipal market volatility in March 2020? In a nutshell, fear and panic. But that’s understandable in the face of a virulent, deadly enemy that you can’t see and is difficult to contain without mass testing. The unknown is menacing, and investors reacted as they have historically — by raising cash and improving liquidity. In many ways, it is similar to the 2008-09 crisis when the bursting housing bubble caused an indiscriminate rush to sell any assets other than Treasuries. What was shocking this time was the unprecedented speed of the sell-off, and the ensuing recovery. Even after 30 years in the business, it was quite alarming.