report by BlackRock

Student of the Market: October 2023

This is a hard commentary to write. The situation is obviously very grave but also extremely fluid and no one has any special or privileged insight as to when a degree of normality may return. All pandemics end but it would be foolish on our part to suggest that it will be over within a few months. What is clear is that the world is tumbling into a serious global recession with significant unemployment. When both supply and demand collapse the end result is obvious and unavoidable. Governments and central banks have thrown several kitchen sinks at the crisis but with a world in lock-down it does little to lift economic activity. Expenses go up but incomes go down.

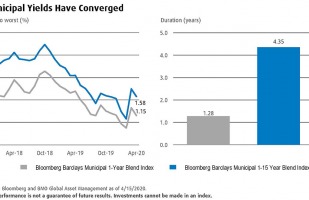

Over the past several weeks, yields between short- and intermediate-term Municipal Bonds have converged. This may be an opportunity for investors to significantly reduce interest rate risk while sacrificing minimal income since shorter-term bonds typically have less sensitivity to rates.

2020 began largely as we expected from an economic perspective, but as the first quarter ended it was difficult even to remember what “normal” economic times looked like, that is, before COVID-19 mushroomed and became a global health crisis.

Before the situation deteriorated in late February, many economists expected the economic effects of the virus to be primarily felt in the first and second quarters with a “v-shaped” recovery to follow. Now many expect a “u-shaped” recovery occurring perhaps by year-end. Economic indicators can lag the headlines, but U.S. unemployment had already begun to spike as the first quarter ended with more to come, likely climbing to double digits as large segments of the economy remain shut down in an effort to contain the virus. We have seen second-quarter annualized GDP estimates ranging from -5% to -30%, but the unprecedented combination of a pandemic and the modern global economy makes this very difficult to call. The numbers will be painful, regardless of the precise magnitude. In terms of the human cost, the pain is already acute.

Credit markets have seen extreme repricing over the past month as a result of the market stress caused by coronavirus and its impact to the economy. The period through March 26 saw some of the most aggressive corporate spread widening in history, with the worst days experiencing almost twice as much widening as any day in 2008. Global investment grade corporate credit spreads reached 340 basis points after having started the year at 102, and we saw global high yield spreads widen past 1,000 basis points as an index, which is generally the level considered the threshold for individual bonds to be considered part of distressed indices.

As the global spread of COVID-19 continues, the United States’ timeline to practice social distancing has now been extended through the end of April. The crisis continues to evolve, leading to questions of how long the social distance measures will remain, how severe will the infection rate get, and when will peak cases be reached. Gauging the length of these measures is crucial to anticipate the economic impacts to U.S. businesses and consumers.

Initiatives such as Veganuary and meat-free Mondays are a sign of how patterns of food consumption are changing. People are increasingly aware that their eating habits can come with dramatic environmental and social costs. As investors, we are particularly interested in how companies are managing ESG risks in both their operations and supply chains, as well as whether they are seeking opportunities in high-growth areas such as vegan protein.

After falling the previous two weeks, stock prices rebounded last week due to increasing optimism over prospects for re-opening the economy.

What caused the extreme municipal market volatility in March 2020? In a nutshell, fear and panic. But that’s understandable in the face of a virulent, deadly enemy that you can’t see and is difficult to contain without mass testing. The unknown is menacing, and investors reacted as they have historically — by raising cash and improving liquidity. In many ways, it is similar to the 2008-09 crisis when the bursting housing bubble caused an indiscriminate rush to sell any assets other than Treasuries. What was shocking this time was the unprecedented speed of the sell-off, and the ensuing recovery. Even after 30 years in the business, it was quite alarming.

Sharing helpful data like decade-returns of the market can motivate investors to focus on the long-term and avoid costly behavioral mistakes.

It is one thing to understand we are living through an unprecedented, pandemic driven economic downturn, and all together another to learn the US unemployment rate is 14.7% and that 20.5 million of our fellow Americans lost their jobs in April.