report by BlackRock

Student of the Market: October 2023

The money, that is. Despite massive stimulus, lending and spending have yet to perk up.

The Fed has been outspoken against negative rates, and a U-shaped recovery could shorten the period they are pinned to zero.

And investors may find some by including a balanced approach in their portfolios.

Read the Weekly Market Snapshot to stay up-to-date with stock markets and sectors, bond market returns and financial news for the week.

Today’s market has eclipsed both the Global Financial Crisis and Tech Bubble in terms of the underperformance of value investing - this call is an opportunity to hear directly from the investment team how BMO interprets these events and reacts to them via proprietary tools and processes.

In our view, the markets feel much healthier at the end of April than a month ago, but underappreciated in the improved sentiment is not only the scale of March policy action, but its continuation into April. Actions announced in April would ordinarily have remained in headlines and discussion for weeks, but the nearly half trillion dollar U.S. fiscal stimulus package has been treated almost as a footnote to its much larger cousin in March. Similarly, Fed and other central banks not only continued to implement the massive programs initiated last month, but significantly expanded on them.

As the first country to tackle COVID-19, China has institutional investors globally wondering about the local situation – and what it means for their portfolios. June Lui, Portfolio Manager, BMO LGM Investments, gives an on-the-ground assessment of China’s economic backdrop and the impact on stocks.

This is a hard commentary to write. The situation is obviously very grave but also extremely fluid and no one has any special or privileged insight as to when a degree of normality may return. All pandemics end but it would be foolish on our part to suggest that it will be over within a few months. What is clear is that the world is tumbling into a serious global recession with significant unemployment. When both supply and demand collapse the end result is obvious and unavoidable. Governments and central banks have thrown several kitchen sinks at the crisis but with a world in lock-down it does little to lift economic activity. Expenses go up but incomes go down.

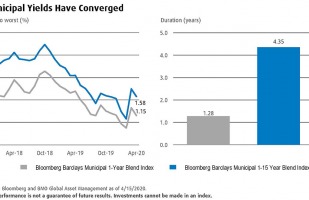

Over the past several weeks, yields between short- and intermediate-term Municipal Bonds have converged. This may be an opportunity for investors to significantly reduce interest rate risk while sacrificing minimal income since shorter-term bonds typically have less sensitivity to rates.

2020 began largely as we expected from an economic perspective, but as the first quarter ended it was difficult even to remember what “normal” economic times looked like, that is, before COVID-19 mushroomed and became a global health crisis.

Before the situation deteriorated in late February, many economists expected the economic effects of the virus to be primarily felt in the first and second quarters with a “v-shaped” recovery to follow. Now many expect a “u-shaped” recovery occurring perhaps by year-end. Economic indicators can lag the headlines, but U.S. unemployment had already begun to spike as the first quarter ended with more to come, likely climbing to double digits as large segments of the economy remain shut down in an effort to contain the virus. We have seen second-quarter annualized GDP estimates ranging from -5% to -30%, but the unprecedented combination of a pandemic and the modern global economy makes this very difficult to call. The numbers will be painful, regardless of the precise magnitude. In terms of the human cost, the pain is already acute.

Credit markets have seen extreme repricing over the past month as a result of the market stress caused by coronavirus and its impact to the economy. The period through March 26 saw some of the most aggressive corporate spread widening in history, with the worst days experiencing almost twice as much widening as any day in 2008. Global investment grade corporate credit spreads reached 340 basis points after having started the year at 102, and we saw global high yield spreads widen past 1,000 basis points as an index, which is generally the level considered the threshold for individual bonds to be considered part of distressed indices.

As the global spread of COVID-19 continues, the United States’ timeline to practice social distancing has now been extended through the end of April. The crisis continues to evolve, leading to questions of how long the social distance measures will remain, how severe will the infection rate get, and when will peak cases be reached. Gauging the length of these measures is crucial to anticipate the economic impacts to U.S. businesses and consumers.